{kind=link}

Given the Risks of a Cashless Society, Why Not Just Keep Cash?

An article on the fintech website Finextra presents a substantial list of challenges faced when implementing a cashless society—including negative impacts on national security and personal privacy—all of which beg the question: why not enjoy the benefits of both cash and cashless options, so everyone can win?

In ‘The challenges of implementing a cashless society’[a], David Hensley of financial consultancy Enryo Limited opens with one of the great problems currently surrounding cashless payments: accessibility. In every country there will be people who do not have a bank account, or are otherwise ineligible to access digital payment methods, for example due to a bad credit rating. Additionally, individuals and businesses alike may struggle to access the required technology and the always-on internet connection required to transact digitally.

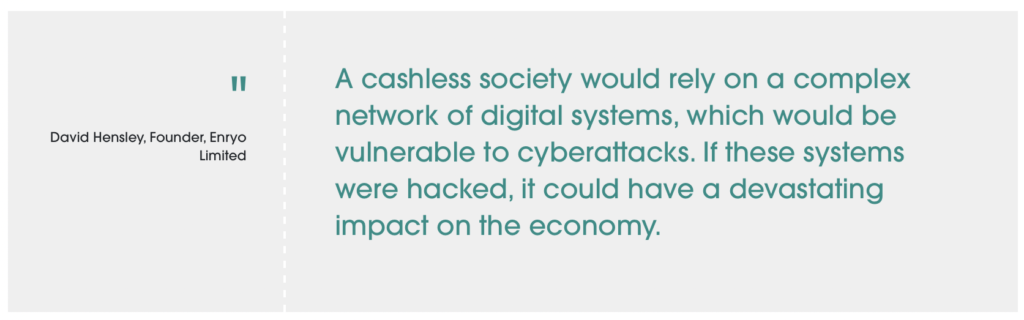

The next challenge highlighted it security. If an economy operated solely on cashless transactions, power or internet outages will bring it to a standstill until services are restored, and cyberattacks would be similarly damaging. In an economy with cash and cashless working together, when the latter is unavailable, people can continue to make essential purchases using cash.

[a] The challenges with implementing a cashless society: https://www.finextra.com/blogposting/24652/the-challenges-with-implementing-a-cashless-society

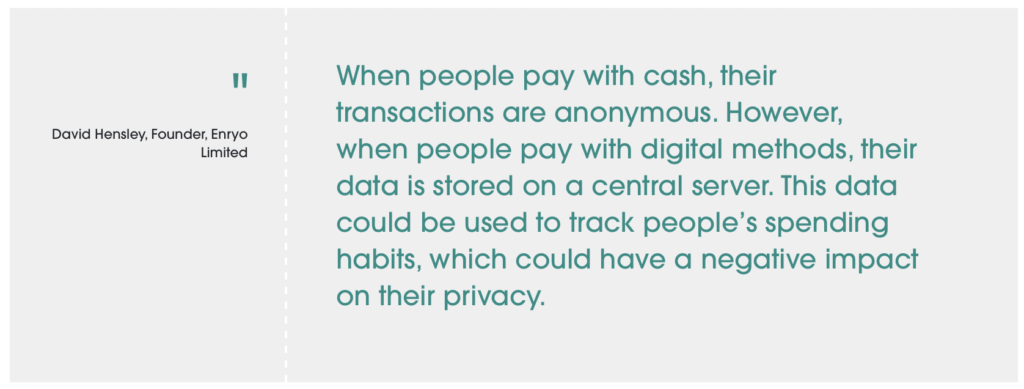

Privacy is the third challenge raised. Cash can be exchanged anonymously, leaving no digital trail. This offers people a choice for any given transaction, enabling them to ask: is this purchase safe and unproblematic to appear on statements and form part of my digital trail? If not, they can use cash. Additionally, with transaction tracking, there is the possibility of financial data being misused, either for fraudulent or other criminal use, or by unscrupulous organisations. In a cashless world, a government could track an individual via their spending, and even cut them off, leaving them unable to pay for goods and services. Even today, cashless spending opens the possibility of analysis by third parties not involved in a transaction. For example, an insurance company could adjust an individual’s premiums based on how much junk food and alcohol they have purchased in the past year.

The fourth challenge is inclusivity, with Hensley pointing out: ‘some economists argue that a cashless society would lead to increased inequality, as the wealthy would be able to benefit from the convenience of digital payments while the poor would be left behind.’ Clearly, this is already an issue, but with cash accessible and usable by all, everyone has the opportunity to participate in the economy. By removing cash, the risk of excluding people becomes unavoidable.

In conclusion, Hensley also mentions cashless payments require infrastructure that may not be available in all parts of all countries, they pose technological challenges—with a need to develop more secure payment methods and ensure systems are fully scalable—and also present social and cultural challenges, with many people currently relying on the tangibility of cash to help them budget [b].

[b] Financial Empowerment Through Cash: https://www.cashmatters.org/blog/financial-empowerment-through-cashHe suggests that ‘despite these challenges, the move towards a cashless society is likely to continue.’ However, there is a critical difference between a future in which cash and cashless options continue to operate side by side, and one in which cash is neither widely accessible nor widely accepted. The former would allow people choice in how they pay and ensure vital low level economic functions could continue in emergencies such as nationwide cyberattacks or natural disasters impacting infrastructure. The latter would depend on 24/7 connectivity and solutions provided by for-profit organisations with agendas, exposing societies to all the risks discussed above.

These points make a strong case for the preservation of payment choice, with the best possible future economy being one which supports both cash and cashless options, harnessing the benefits of each and allowing people the freedom to select how they want to pay on a transaction by transaction basis.

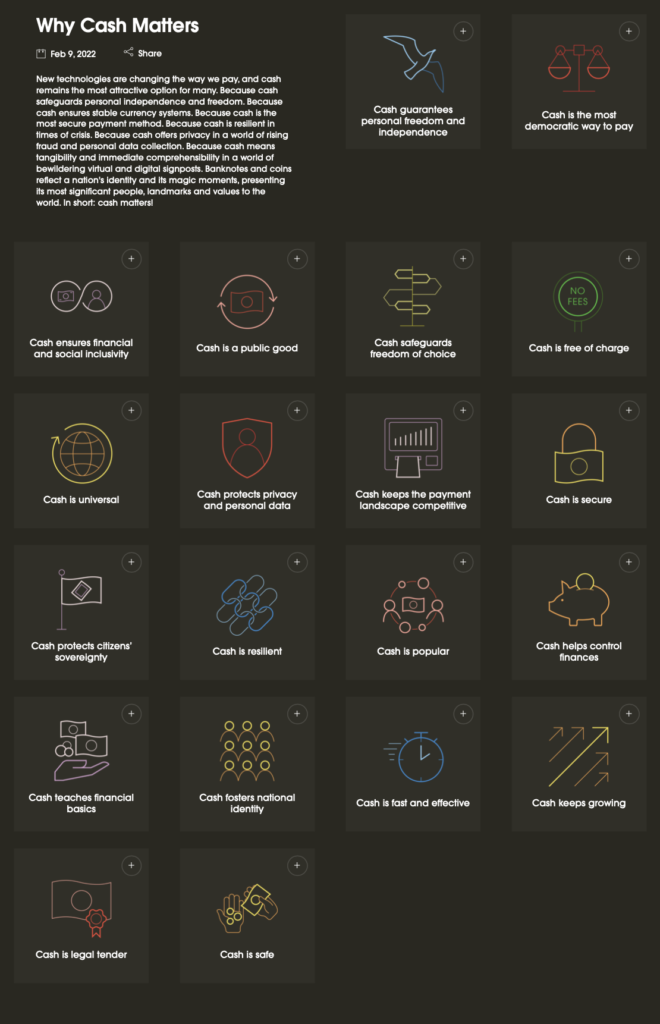

Why Cash Matters

New technologies are changing the way we pay, and cash remains the most attractive option for many. Because cash safeguards personal independence and freedom. Because cash ensures stable currency systems. Because cash is the most secure payment method. Because cash is resilient in times of crisis. Because cash offers privacy in a world of rising fraud and personal data collection. Because cash means tangibility and immediate comprehensibility in a world of bewildering virtual and digital signposts. Banknotes and coins reflect a nation’s identity and its magic moments, presenting its most significant people, landmarks and values to the world. In short: cash matters!

For More Details Click Here [copy and paste]: https://www.cashmatters.org/why-cash-matters-top-20-reasons-for-the-popularity-and-relevance-of-cash

Laws Governing Digital Payment Fraud in India

The exponential rise in digital payments in India has brought convenience to millions of users. However, this shift towards cashless transactions has also led to an increase in digital payment fraud. Addressing these concerns, India has established a comprehensive legal and regulatory framework to safeguard users and maintain trust in digital payment systems.

The exponential rise in digital payments in India has brought convenience to millions of users. However, this shift towards cashless transactions has also led to an increase in digital payment fraud. Addressing these concerns, India has established a comprehensive legal and regulatory framework to safeguard users and maintain trust in digital payment systems. This article delves into the key laws and regulations governing digital payment fraud in India, highlighting the role of regulatory bodies and mechanisms for redressal.

What is Digital Payment Fraud?

Digital payment fraud refers to unlawful acts involving unauthorised access, manipulation, or theft of funds through digital payment channels. These frauds include phishing, identity theft, malware attacks, social engineering, and more. The growth in fraud cases is primarily attributed to increased digital adoption, technological vulnerabilities, and a lack of awareness among users.

Key Regulatory Bodies Governing Digital Payments

India has established several regulatory bodies to oversee and secure the digital payment ecosystem, ensuring accountability and efficiency in combating fraud.

Reserve Bank of India (RBI)

The Reserve Bank of India (RBI) is the apex regulatory body for digital payments in India. It ensures the safety, security, and efficiency of payment systems under the Payment and Settlement Systems Act, 2007. The RBI issues guidelines to minimise fraud risks and mandates robust security measures for digital payment platforms.

Ministry of Electronics and Information Technology (MeitY)

MeitY plays a vital role in fostering a secure digital ecosystem by introducing initiatives like the Digital India Programme and guidelines for cybersecurity. It also collaborates with the RBI and other stakeholders to regulate the digital payment sector effectively.

National Payments Corporation of India (NPCI)

The NPCI oversees the operation of major payment systems, including Unified Payments Interface (UPI), Bharat Bill Payment System (BBPS), and Immediate Payment Service (IMPS). It develops and enforces security standards to protect users from fraud.

Relevant Laws Governing Digital Payment Fraud

These laws provide the legal backbone for addressing and mitigating digital payment fraud in India, ensuring user protection and system integrity.

Payment and Settlement Systems Act, 2007

This act provides a legal framework for the regulation and supervision of payment systems in India. It empowers the RBI to authorise, regulate, and oversee payment system operators. The act ensures the safety and efficiency of digital payment systems and provides mechanisms for dispute resolution in cases of fraud.

Information Technology Act, 2000

The IT Act addresses cybercrimes and provides a legal framework for electronic transactions in India. It includes provisions related to data protection, cybersecurity, and penalties for identity theft, phishing, hacking, and unauthorised access to computer systems. Section 66C and Section 66D of the IT Act specifically deal with identity theft and impersonation, often associated with digital payment frauds.

Consumer Protection Act, 2019

The Consumer Protection Act, 2019, safeguards consumers against unfair trade practices and fraudulent activities, including digital payment frauds. It empowers consumers to file complaints against service providers for lapses in security or fraudulent transactions. The act also establishes e-commerce rules to ensure transparency and accountability in digital transactions.

Prevention of Money Laundering Act, 2002

This act mandates stringent Know Your Customer (KYC) norms for digital payment service providers to prevent fraud and money laundering. It requires service providers to report suspicious transactions to the Financial Intelligence Unit (FIU) and comply with anti-money laundering regulations.

Indian Penal Code (IPC), 1860

Traditional provisions of the IPC [1] are often applied to digital payment frauds. Sections 419 (cheating by impersonation), 420 (cheating and dishonestly inducing delivery of property), and 468 (forgery for the purpose of cheating) are commonly invoked in cases involving digital payment fraud.

[1] https://lawbhoomi.com/category/law-notes/ipc/Regulatory Guidelines to Prevent Digital Payment Fraud

India’s regulatory framework includes proactive measures to mitigate fraud risks and enhance the security of digital payment platforms.

Two-Factor Authentication (2FA)

The RBI mandates two-factor authentication for all online transactions to enhance security. This involves verifying a user’s identity through two separate components, such as a password and a one-time password (OTP).

PCI DSS Compliance

Merchants and payment service providers must adhere to Payment Card Industry Data Security Standards (PCI DSS) to ensure the protection of cardholder data during transactions. These guidelines help prevent data breaches and enhance trust among users.

Data Protection and Privacy Guidelines

The Draft Digital Personal Data Protection Bill, 2022, aims to govern the collection, storage, and processing of personal data. It introduces stricter norms for digital payment service providers, ensuring that user data is not misused or exposed to risks.

Security Standards for UPI and Wallets

The NPCI has issued specific guidelines for UPI and mobile wallets, focusing on encryption, user verification, and fraud monitoring. Regular audits and compliance checks are conducted to ensure adherence to these standards.

What are the Mechanisms for Addressing Digital Payment Fraud

Several mechanisms have been put in place to ensure swift action and redressal in cases of digital payment fraud.

Grievance Redressal Mechanisms

Digital payment platforms are required to set up robust grievance redressal mechanisms to address user complaints effectively. The RBI’s Ombudsman Scheme for Digital Transactions allows users to escalate unresolved complaints related to digital payments.

Cyber Crime Reporting Portal

The Ministry of Home Affairs has launched the Cyber Crime Reporting Portal (“cybercrime.gov.in”)[2], enabling users to report digital payment frauds and other cybercrimes. This portal streamlines the process of filing complaints and tracking their status.

[2] http://cybercrime.gov.in/Consumer Courts

Victims of digital payment fraud can approach consumer courts under the Consumer Protection Act to seek redressal and compensation. The process involves filing a complaint against the service provider for lapses in security or fraudulent activities.

Challenges in Combating Digital Payment Fraud

Despite a strong regulatory framework, challenges persist in addressing and preventing digital payment fraud in India.

Lack of Awareness

A significant portion of the population remains unaware of the risks associated with digital payments and the precautions required to prevent fraud. This makes them vulnerable to phishing and other fraudulent activities.

Technological Vulnerabilities

Despite stringent regulations, technological vulnerabilities in payment systems can be exploited by cybercriminals. Regular updates and robust security protocols are essential to mitigate these risks.

Low Adoption of Cybersecurity Measures

Many small merchants and service providers fail to implement adequate cybersecurity measures due to a lack of resources or awareness. This creates loopholes in the system, increasing the risk of fraud.

Measures to Improve Digital Payment Security

Strengthening the security and awareness around digital payments is crucial to minimising risks and protecting users.

User Education

Awareness campaigns by regulatory bodies and service providers can educate users about safe practices, such as verifying payment links, avoiding public Wi-Fi for transactions, and monitoring account activity regularly.

Strengthening Cyber Laws

Updating existing laws and introducing stricter penalties for digital payment fraud can deter cybercriminals and enhance user confidence in digital payment systems.

Collaboration Among Stakeholders

Collaboration between regulatory bodies, financial institutions, and technology providers can create a more secure and efficient digital payment ecosystem. Sharing threat intelligence and best practices can help mitigate risks.

Nevertheless, it is essential to sustain the presence of cash.

Source: Cashmatters, Lawbhoomi,

Also Read:

Also Watch: